Executive Summary

- Apple is set to disrupt the established hierarchy of the PC industry by becoming the third-largest laptop vendor by late 2026. This ascent, largely attributed to the successful launch of the affordable ‘MacBook Neo’ line, signifies Apple’s pivot from a niche premium player to a high-volume market leader, directly challenging Dell’s long-standing dominance.

Strategic Deep-Dive

The MacBook Neo Catalyst: Analyzing Apple’s Ascent to the Global Top Three

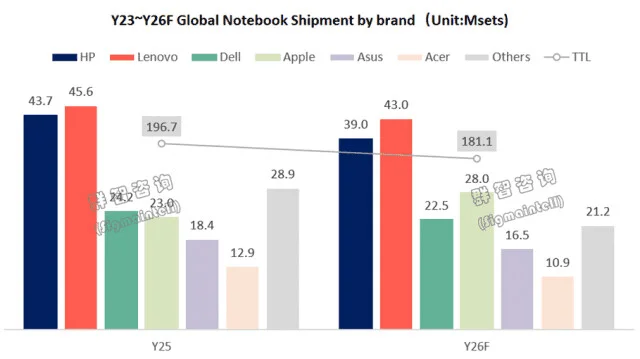

Apple is on the verge of achieving what many industry analysts once thought impossible: becoming a volume leader in the global PC market. According to recent projections from Sigmaintell, a leading market intelligence firm, Apple is on track to displace Dell as the world’s third-largest laptop vendor by the end of 2026. This milestone represents a tectonic shift in the industry, marking the first time a premium-focused, proprietary-OS manufacturer has successfully scaled its way into the top tier of what has traditionally been a Windows-dominated commodity market.

The strategic engine behind this growth is the ‘MacBook Neo.’ For years, Apple’s entry-level offerings—most notably the MacBook Air—were still priced at a premium relative to the vast majority of consumer laptops. The Neo line represents a fundamental shift. By leveraging the cost efficiencies of its vertically integrated Apple Silicon architecture, Apple has introduced a device that competes aggressively on price without sacrificing the battery life and build quality that define its brand.

This ‘MacBook for the masses’ strategy has tapped into a massive reservoir of latent demand among students, emerging market professionals, and enterprise fleets that were previously locked into the Dell or HP ecosystems for budgetary reasons.

From a competitive landscape perspective, Apple’s move into the number three spot is a direct challenge to the traditional business models of legacy PC makers. Dell, in particular, has long relied on its strength in the corporate sector and its supply chain mastery to maintain volume. However, the MacBook Neo is eroding these advantages.

Apple’s ability to offer a unified software and hardware experience—coupled with the long-term cost benefits of lower IT support needs and higher resale value—is making the Mac ecosystem increasingly attractive to procurement managers. As Apple increases its market share, the network effects of its ecosystem strengthen, making it harder for users to switch back to Windows-based alternatives.

Furthermore, the data suggests that Apple is using hardware volume as a vehicle for its high-margin services business. Every MacBook Neo sold represents a new portal for iCloud subscriptions, Apple Arcade, and App Store transactions. This ‘Trojan Horse’ strategy allows Apple to be more aggressive with hardware pricing than competitors who rely solely on hardware margins to survive.

As Apple approaches the third-place position, it is essentially changing the rules of the game from a hardware specification race to an ecosystem lock-in race. For Dell and HP, the threat is existential; they are no longer just competing against a laptop, but against a global platform that spans from the pocket to the desktop.

In conclusion, Apple’s projected rise to the third-largest vendor is the culmination of a decade-long transition toward silicon independence. By controlling its own destiny through M-series chips, Apple has gained the financial and technical flexibility to attack the mid-market with surgical precision. As we look toward 2026, the question is no longer whether Apple can maintain its premium status, but how high its ceiling can go in a market it is rapidly redefining.

The ‘MacBook Neo’ era signifies that Apple is no longer content with being the most profitable player in the room; it now intends to be the most prevalent.