🔍 Executive Summary

- The memory OSAT sector is facing a complex Q2 2026 landscape where record-high capacity utilization is being countered by significant price hikes in upstream substrate materials.

Strategic Deep-Dive

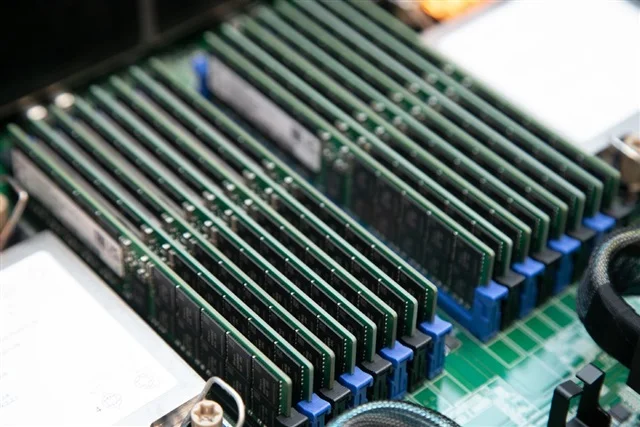

The global memory sector in 2026 is witnessing a fascinating economic paradox where record-breaking demand is creating its own set of supply chain challenges. Following a surprisingly robust first quarter, memory Outsourced Semiconductor Assembly and Test (OSAT) providers are entering the second quarter with near-full capacity utilization. This momentum is largely sustained by the relentless appetite for high-density DRAM from hyperscalers and AI data center operators.

However, as utilization rates plateau at their upper limits, the focus of the industry is shifting toward the rising costs of upstream materials, particularly semiconductor substrates.

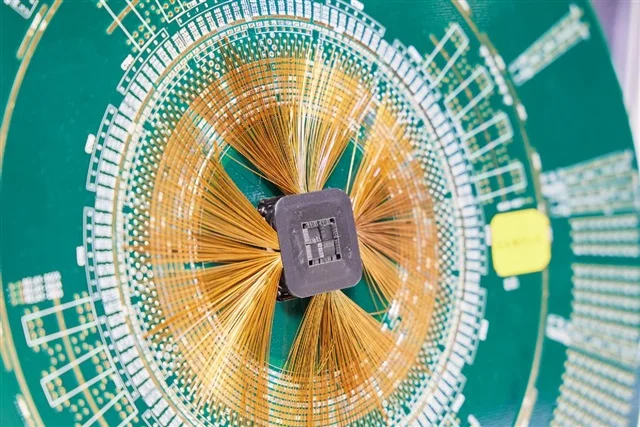

Substrate price hikes are expected to become a dominant trend in Q2 2026. High-end substrates, such as Flip-Chip Ball Grid Array (FC-BGA) and multi-layer substrates used in advanced DDR5 and HBM modules, are seeing extended lead times and aggressive pricing from vendors. This is a direct result of the scarcity of core dielectric materials and the increased complexity required for high-speed signal integrity.

For OSAT providers, this creates a significant margin squeeze. While high utilization generally allows for better fixed-cost absorption, the sharp rise in raw material costs requires either successful price passthroughs to chipmaker clients or an optimization of the utilization-vs-yield trade-off. Firms that can maintain high yields even at peak utilization will be best positioned to weather these inflationary pressures.

From a strategic perspective, the current market dynamic is leading to a consolidation of bargaining power among the top-tier OSAT players who have secured long-term supply agreements for substrates. In contrast, smaller players are finding it increasingly difficult to compete for limited material allocations, potentially leading to a ‘K-shaped’ recovery within the memory backend sector. This cycle is also pushing OSATs to invest more heavily in automation and advanced testing protocols to minimize waste and maximize the value of each expensive substrate.

As we progress through 2026, the resilience of the memory supply chain will be tested by these cost pressures. For global investors and analysts, the key metrics to watch will be the substrate inventory levels and the ability of OSATs to maintain profitability amidst the dual forces of high demand and rising production costs. The memory upswing is real, but its profitability is increasingly tied to the mastery of the upstream supply chain.