🔍 Executive Summary

- The global memory semiconductor market is entering a period of structural supply-demand imbalance. Samsung Electronics and SK hynix have issued stark warnings that High Bandwidth Memory (HBM) shortages will persist until at least 2027. With major customers pre-booking supply years in advance, the allocation of production lines to HBM is tightening the broader DRAM market, driving prices higher and setting the stage for record-breaking profitability for the South Korean giants.

Strategic Deep-Dive

The global memory semiconductor industry is navigating a seismic shift as Samsung Electronics and SK hynix, the dual titans of the sector, signal a long-term structural shortage of High Bandwidth Memory (HBM). During recent industry summits, executives from both firms clarified that the insatiable demand for generative AI training and inference is outstripping manufacturing capacity at a rate that suggests equilibrium will not be reached until at least 2027. From the perspective of a data systems architect, the ‘memory wall’ has become the primary constraint in AI scalability; without sufficient HBM bandwidth, even the most advanced GPUs remain underutilized.

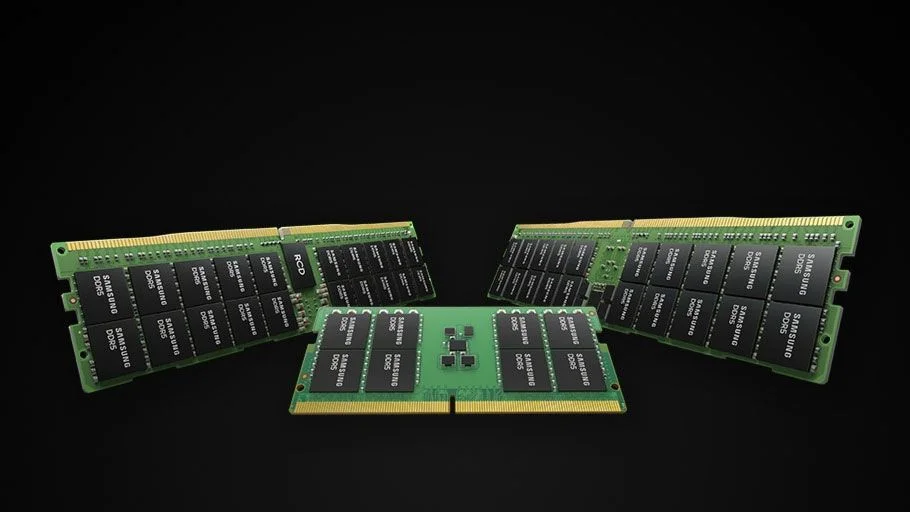

This shortage is exacerbated by the technical complexity of HBM manufacturing. Unlike standard DRAM, HBM requires vertical stacking of multiple dies using Through-Silicon Via (TSV) technology. The process is fraught with yield challenges, particularly as the industry transitions from HBM3e to the next-generation HBM4 standard, which will likely involve hybrid bonding and the integration of the base die directly onto the GPU foundry process.

The manufacturing footprint required for HBM is also significantly larger—roughly three times that of standard DRAM for the same bit density. Consequently, as Samsung and SK hynix reallocate their cleanest wafer capacity to HBM, the supply of general-purpose DRAM for PCs, smartphones, and traditional servers is tightening. This ‘supply cannibalization’ is a deliberate strategic move to prioritize high-ASP (Average Selling Price) products, but it has the secondary effect of inflating prices across the entire DRAM market, ensuring record-breaking profitability for the foreseeable future.

Major hyperscalers and AI hardware OEMs have responded by abandoning traditional just-in-time procurement in favor of long-term reservation contracts, some stretching into late 2026 and early 2027. However, senior journalists and market analysts remain wary of the ‘Double Ordering’ phenomenon—a classic semiconductor cycle trap where customers inflate orders to ensure a minimum allocation, potentially leading to a market correction if AI demand eventually plateaus. Despite these risks, the roadmap for HBM4 and the emergence of ‘Custom HBM’ indicate that memory is no longer a commodity but a specialized logic-like component.

For Samsung and SK hynix, the challenge lies in managing this unprecedented growth without overextending capital expenditure to a point of future vulnerability. As the industry approaches the 2027 milestone, the focus will remain on yield optimization and the transition to 12-layer and 16-layer stacks, ensuring that the ‘memory bottleneck’ does not stall the global AI revolution.