🔍 Executive Summary

- Huawei is positioning itself as the 'Nvidia of China,' targeting a massive $12 billion in AI chip revenue as domestic tech giants pivot toward the Ascend ecosystem amid US export controls.

Strategic Deep-Dive

Huawei’s $12 Billion Ascendancy: A Strategic Masterstroke

Huawei is set to redefine the geopolitical landscape of the semiconductor industry with an ambitious $12 billion revenue target for its AI chip division this year. According to the Financial Times, this represents a staggering 60% growth rate compared to the previous year. This rapid ascent is a direct consequence of the escalating trade war between the United States and China.

As the U.S. continues to tighten export controls on Nvidia’s flagship H100 and B200 GPUs, Chinese tech giants—including Alibaba, Tencent, and Baidu—have been forced to accelerate their decoupling from Western silicon. Huawei has stepped into this void, positioning its Ascend AI series not just as a temporary workaround, but as a permanent, high-performance foundation for China’s AI future.

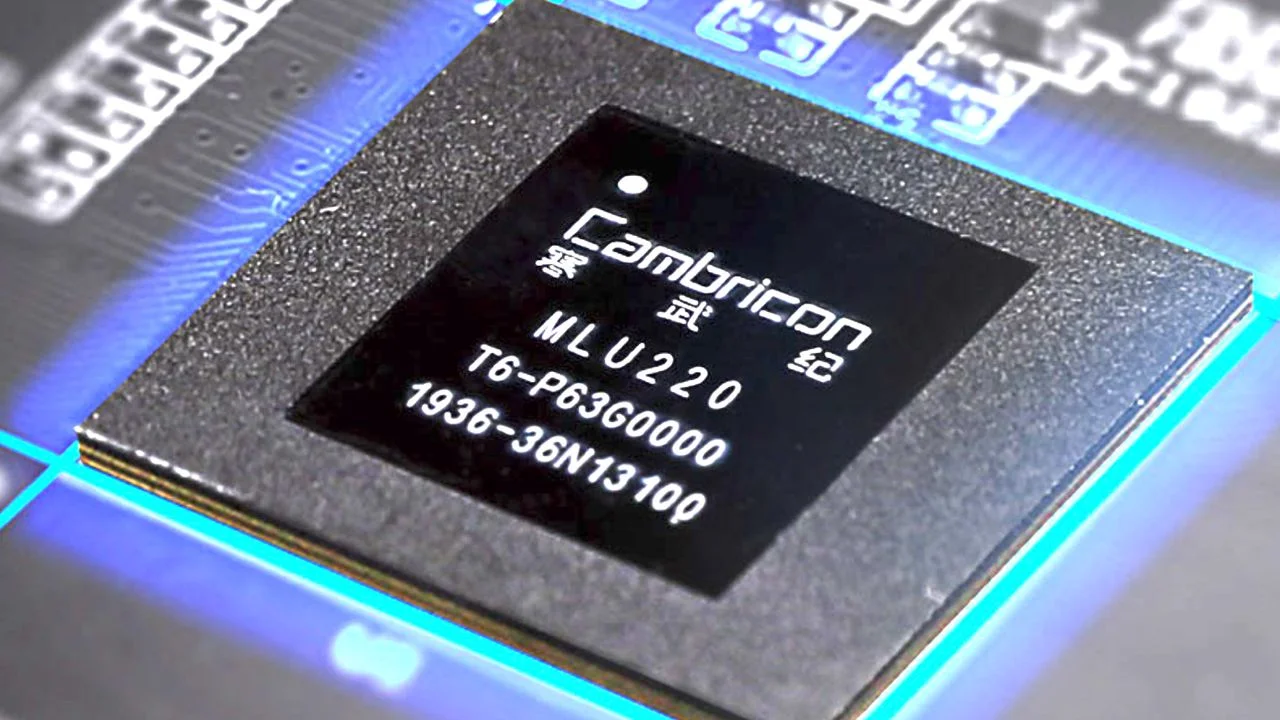

Technical Parity: Ascend 910B and the CANN Ecosystem

From a technical perspective, the heavy lifting is being done by the Ascend 910B processor. While Huawei faces significant challenges in accessing the latest sub-5nm lithography nodes due to sanctions, the company has compensated through architectural ingenuity and domestic manufacturing partnerships. The Ascend 910B is increasingly viewed by Chinese engineers as the most viable alternative to Nvidia’s A100/H100 class hardware, especially when compared to the ’nerfed’ versions Nvidia is permitted to export to China (like the H20).

However, hardware is only half the battle. Huawei’s true competitive edge lies in CANN (Compute Architecture for Neural Networks), its proprietary software stack that mirrors Nvidia’s CUDA. CANN provides the necessary libraries and compiler tools to allow AI developers to port their large language models (LLMs) from Nvidia to Huawei with minimal friction.

This software-first approach is the primary reason why Chinese cloud providers are now ordering tens of thousands of Ascend units annually.

Economic and Geopolitical Displacement of Nvidia

If Huawei successfully hits its $12 billion sales target, it will effectively become the ‘Nvidia of China,’ controlling the single largest domestic market for AI acceleration. This shift represents a massive loss of high-margin revenue for Nvidia and potentially signals a permanent change in market dynamics. The more Chinese firms invest in the Huawei ecosystem, the more robust the CANN library becomes, creating a powerful network effect that makes it harder for Western firms to re-enter the market even if sanctions were eased.

Furthermore, Huawei’s aggressive growth suggests that the ‘Silicon Divide’ is no longer a theoretical risk but a present reality. China is successfully building a vertically integrated, self-sufficient AI stack—spanning from internal chip design and OS development to high-end cloud services—that operates entirely outside of the U.S.-led semiconductor supply chain.

The Road Ahead: Overcoming Manufacturing Bottlenecks

The ultimate test for Huawei will be its ability to scale production. Hitting $12 billion in revenue implies a massive increase in wafer starts. While China’s domestic foundries, like SMIC, have made strides in 7nm and 5nm-class production, the yields and volume remain a closely guarded secret.

Huawei’s shift toward chiplet-based designs is a logical architectural response to these manufacturing constraints, allowing them to stitch together smaller, high-yield dies to create a high-performance logic processor. As Huawei secures its dominance in China, the next phase of its strategy will likely involve exporting this localized AI ecosystem to other regions within the Global South, creating a secondary global technology sphere. For the global tech industry, Huawei’s $12 billion milestone is a clarion call: the era of American silicon dominance is being challenged by a formidable, state-supported domestic rival with near-infinite demand in its home market.