🔍 Executive Summary

- As the AI chip race hits a CoWoS-induced supply ceiling, the industry is shifting toward a 'packaging-first' design philosophy. With MediaTek seeking new expertise to navigate TSMC’s capacity limits, a critical question emerges: Can Intel’s foundry services (IFS) deliver the high-yield advanced packaging needed to disrupt the status quo?

Strategic Deep-Dive

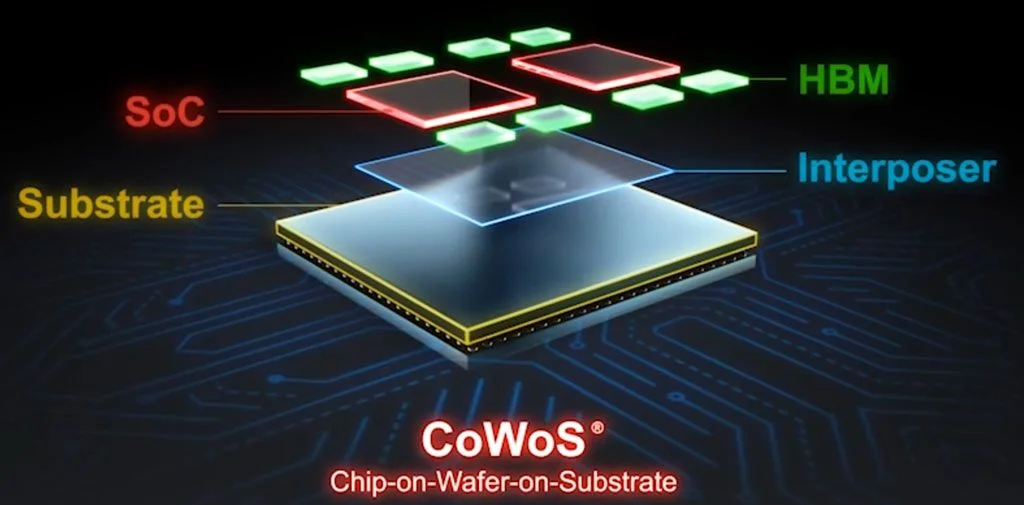

The AI semiconductor sector has reached a critical pivot point where raw compute power is no longer the sole differentiator. The industry has encountered a formidable new bottleneck: advanced packaging. Specifically, the acute supply constraints surrounding TSMC’s CoWoS (Chip on Wafer on Substrate) technology have become the primary strategic hurdle for high-performance chip designers like MediaTek.

This scarcity has triggered a fundamental shift in semiconductor design philosophy, moving toward a ‘packaging-first’ paradigm.

In this new era, the architecture of an AI accelerator is defined by its interconnect density and bandwidth rather than just transistor scaling. The urgent need to integrate disparate chiplets with minimal latency has turned packaging from a back-end process into a front-end strategic asset. MediaTek’s recent tactical hires in the packaging domain underscore a broader industry desperation to secure alternative supply chains.

This leads to the industry’s most pressing question: Can Intel deliver? Intel’s Foundry Services (IFS) are being scrutinized as the most viable relief valve for the global CoWoS crunch.

For Intel, the current supply vacuum presents a unique window of opportunity to establish itself as a primary alternative in the advanced packaging ecosystem. By offering heterogeneous integration services that rival TSMC’s CoWoS, Intel could potentially decouple chip designers from their total reliance on a single vendor. However, the challenge remains one of execution.

Intel must demonstrate consistent, high-yield production at scale to win the trust of Tier-1 clients. If Intel succeeds, it could reshape the competitive dynamics of the global foundry market, transforming the CoWoS bottleneck into a springboard for its own foundry resurgence. The next two years will determine if Intel can transition from a technology architect to a reliable high-volume packaging provider for the AI era.