🔍 Executive Summary

- Nvidia CEO Jensen Huang has officially acknowledged that US export controls have effectively eliminated the company's market share in China's critical data-center sector.

- In response to this displacement, Beijing is accelerating a massive state-led effort to achieve semiconductor sovereignty, targeting every layer from silicon wafers to AI accelerators.

- The primary challenge for Chinese firms remains the development of a software ecosystem capable of rivaling Nvidia's CUDA, which has historically been the barrier to entry for domestic alternatives.

Strategic Deep-Dive

Geopolitical Displacement: The Technical Ramifications of Nvidia’s China Exit

In a landmark admission, Nvidia CEO Jensen Huang has confirmed that the company’s market share in the Chinese data-center computing sector has been effectively reduced to zero. This total displacement is the direct result of escalating US Department of Commerce export controls, which have transitioned from restricting specific high-end chips to a broader blockade of the computational performance required for modern LLM (Large Language Model) training. For Nvidia, this marks the end of an era in one of its most lucrative territories; for China, it marks the beginning of a desperate race for technological self-sufficiency.

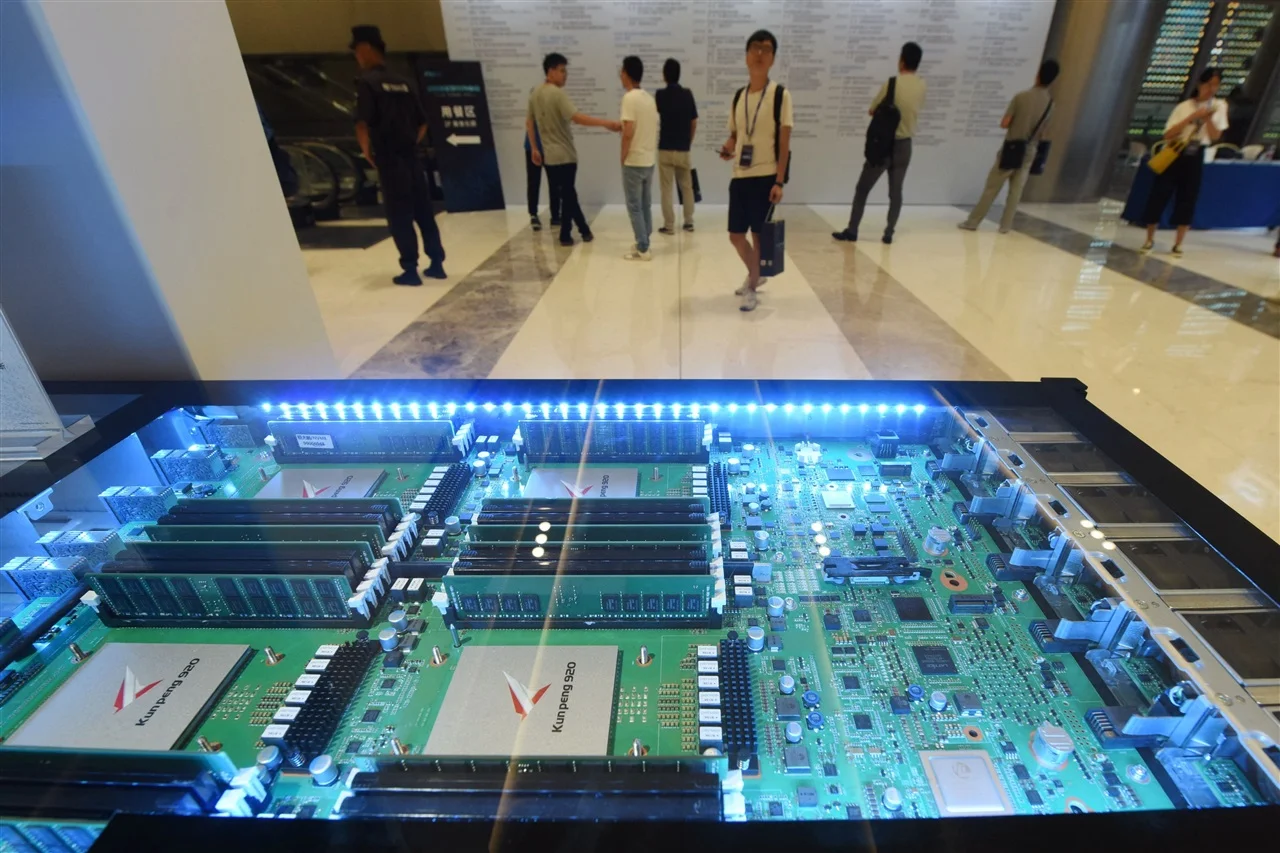

Filling the Void: The Drive for Full-Stack Localization

Beijing’s response to the absence of Nvidia is no longer characterized by mere mimicry. Instead, the Chinese government is funding a comprehensive ‘Full-Stack Localization’ strategy. This involves a multi-layered approach to secure the semiconductor supply chain from the ground up:

- Upstream Material Sovereignty: Massive investments are flowing into the production of high-quality silicon wafers and specialized chemicals. By controlling the raw materials, China aims to insulate its domestic fabrication facilities from further external sanctions.

- Architectural Divergence: With access to Nvidia’s architecture cut off, Chinese firms are pivoting toward RISC-V and proprietary AI accelerator designs. The goal is to produce domestic chips that can match the TFLOPS (Teraflops) performance of Western counterparts, even if manufactured on less efficient process nodes.

- The CUDA Challenge: Perhaps the most significant hurdle is Nvidia’s CUDA software ecosystem. Chinese tech giants are collaborating on unified software abstraction layers to allow developers to port AI workloads from CUDA to domestic hardware without prohibitive latency or retraining costs.

Commercial and Strategic Consequences

The zero-market share reality for Nvidia signals a permanent bifurcation of the global AI industry. We are witnessing the emergence of a ‘Great Firewall of Silicon,’ where Chinese AI development will increasingly rely on localized, vertically integrated stacks. While this ensures China’s survival against sanctions, it also risks creating a technological island.

For global chipmakers, the challenge is now one of risk management: navigating a world where the second-largest economy is effectively a ’no-go zone’ for Western high-performance computing products, forcing a total re-evaluation of long-term revenue models and R&D pipelines.