🔍 Executive Summary

- Major manufacturers like Samsung and Micron are exiting the mature 2D NAND market, triggering panic buying and sharp price increases. Industry sources predict a prolonged shortage, likely leading to polarized product specifications in the secondary market.

Strategic Deep-Dive

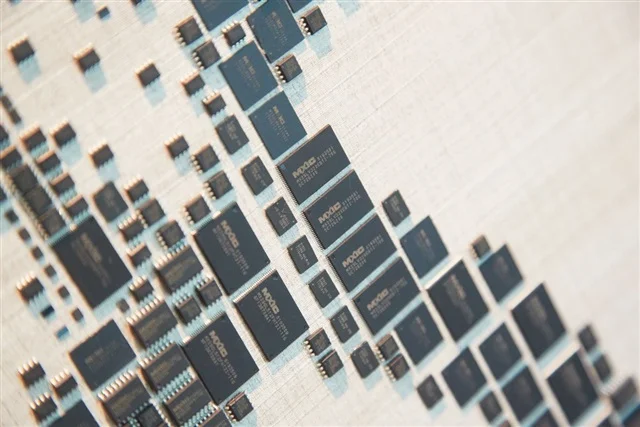

The global semiconductor landscape is witnessing a structural collapse in the mature 2D NAND market, a sector previously deemed stable but now fraught with unprecedented volatility. As industry titans Samsung Electronics and Micron Technology accelerate their strategic pivot toward high-density 3D NAND and AI-centric memory architectures, the legacy 2D NAND ecosystem is being left in a precarious vacuum. This shift is not merely a routine product cycle transition; it represents a fundamental decommissioning of the infrastructure required to produce Single-Level Cell (SLC) and Multi-Level Cell (MLC) 2D NAND, which remains critical for specific industrial niches.

The technical rationale for 2D NAND’s persistence in these sectors lies in its physical reliability. Unlike the charge-trap technology used in vertically stacked 3D NAND, 2D floating-gate architectures offer superior electron retention and P/E (Program/Erase) cycle endurance, making them indispensable for automotive engine control units (ECUs), aerospace signaling systems, and medical diagnostics where failure is not an option.

According to the latest intelligence, the market response to this withdrawal has been characterized by aggressive ‘panic buying.’ Large-scale hardware integrators and industrial OEMs, realizing that the window for securing long-term supply is closing, have entered a bidding war for remaining inventories. This has catalyzed a sharp spike in average selling prices (ASPs), with some legacy parts seeing 50-100% premiums in the spot market. The difficulty in resolving this shortage is rooted in the physics of fabrication.

Modernizing a fab for 3D NAND involves changing the entire toolset for high-aspect-ratio etching and chemical vapor deposition. Once a line is converted, reverting to the planar processes of 2D NAND is economically prohibitive. Therefore, the current scarcity is likely permanent, signaling a ‘supply-side shock’ that cannot be mitigated by standard capacity expansions.

As the industry moves forward, we anticipate a deepening ‘polarization’ of hardware specifications. On the high end, enterprises will be forced to undergo costly platform migrations, redesigning their storage controllers to accommodate the different voltage requirements and error-correction code (ECC) complexities of 3D TLC or QLC NAND. On the lower end, budget-constrained sectors may be forced to source from secondary or tertiary vendors who lack the stringent quality controls of the majors, potentially leading to a decline in overall hardware reliability.

For the global technology analyst, this situation highlights a critical vulnerability in the hardware supply chain: the over-reliance on a handful of suppliers who can, through a single strategic pivot, render entire categories of industrial equipment obsolete. The move toward alternative solution-seeking is no longer a peripheral strategy but a central requirement for business continuity in a market where legacy support is rapidly evaporating. The resulting price volatility is expected to ripple through the consumer electronics and industrial machinery sectors for the next several fiscal quarters, forcing a re-evaluation of long-term component sourcing and lifecycle management.