🔍 Executive Summary

- Surging demand for high-performance PCBs in AI semiconductors is tightening the supply of Copper Clad Laminate (CCL), leading to lead times extending more than twofold. This upstream supply crunch poses a risk to the entire downstream hardware assembly timeline.

Strategic Deep-Dive

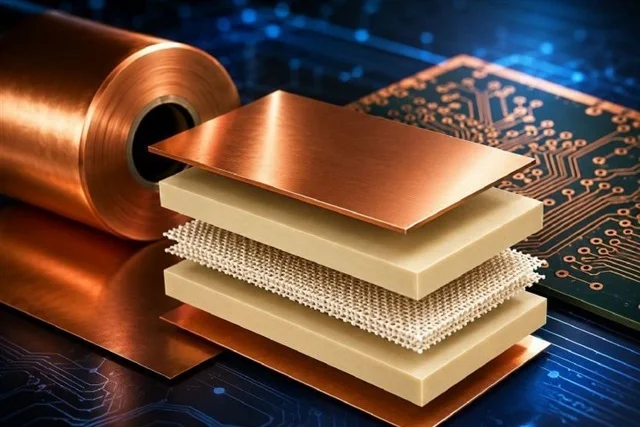

The semiconductor industry’s unrelenting push toward artificial intelligence integration has exposed a critical vulnerability in the electronics value chain: the supply of advanced Copper Clad Laminates (CCL). As the fundamental building block of Printed Circuit Boards (PCBs), the CCL market is currently undergoing a period of extreme duress, with lead times extending more than twofold—from a standard 4-6 weeks to over 12-14 weeks in many cases. This upstream supply crunch is driven by the soaring demand for high-layer-count (HLC) and high-density interconnect (HDI) substrates required for AI accelerators and enterprise-grade servers.

For global technology analysts, this material shortage is the ‘canary in the coal mine’ for broader hardware assembly delays and inflationary pressures.

The technical specifications for AI-grade CCL are significantly more demanding than those for consumer electronics. To support high-frequency signals exceeding 112G or 224G per lane, the laminates must exhibit ‘Ultra-Low Loss’ (ULL) characteristics, defined by extremely low Dielectric Constants (Dk) and Dissipation Factors (Df). Achieving these properties requires sophisticated resin formulations—often involving polytetrafluoroethylene (PTFE) or modified polyphenylene ether (PPE)—and specialized glass fabrics that minimize signal degradation and impedance mismatch.

Furthermore, the thermal management requirements for AI chips, which can operate at upwards of 700W to 1000W TDP, necessitate substrates with superior Glass Transition Temperatures (Tg) and high Thermal Conductivity. Upstream suppliers are struggling to maintain high yields for these complex formulations, and the capital expenditure required to expand production for high-grade CCL is substantial, preventing a quick resolution to the supply deficit.

As lead times continue to expand, the ripple effect is being felt across the entire hardware ecosystem. PCB manufacturers are facing a backlog of orders, as they cannot begin the lamination process without the core CCL material. This, in turn, creates a downstream bottleneck for system integrators who are awaiting the motherboards and interposers necessary to house GPU clusters.

The current environment has shifted the power dynamic toward material scientists and upstream chemical suppliers. Major hardware OEMs are now being forced to engage in ‘pre-emptive sourcing’ and long-range forecasting, often securing material months before final designs are even frozen. This scarcity also risks triggering a cost-push inflation cycle, as the price of high-performance resins and copper foils rises in tandem with demand.

If the CCL bottleneck is not alleviated through strategic capacity investments or material innovation, it could become the primary limiting factor for the physical rollout of the next generation of AI data centers. The current crisis underscores the absolute necessity for a vertically integrated supply chain strategy where raw material availability is treated with the same strategic priority as silicon architecture.