🔍 Executive Summary

- The AI-driven semiconductor shortage has pushed SK hynix to a total depletion of inventory and production slots, forcing Tier-1 customers to bypass traditional procurement in favor of direct infrastructure funding and equipment purchasing to guarantee future supply.

Strategic Deep-Dive

The global semiconductor landscape is witnessing a radical and arguably permanent transformation as the demand for AI-specific memory hardware, particularly High Bandwidth Memory (HBM), outstrips existing production capabilities. According to industry analysis, SK hynix has reached a critical juncture where its available memory capacity has effectively hit zero. This total depletion of inventory and production slots has triggered a wave of desperation among Tier-1 technology customers who find that standard long-term supply agreements (LTAs) are no longer sufficient to guarantee the silicon necessary for their next-generation AI clusters.

In a shift that rewrites the manual of semiconductor procurement, these clients are now moving beyond purchase orders to directly funding the ‘bricks and mortar’ of the production floor.

This trend represents a total collapse of the traditional arms-length relationship between chipmakers and their buyers. Under normal market conditions, a manufacturer like SK hynix would bear the massive capital expenditure (CapEx) risk of building new facilities and purchasing lithography tools, recouping the investment through years of chip sales. However, the current AI-driven vacuum is so severe that customers are willing to inject hundreds of millions of dollars directly into SK hynix’s infrastructure.

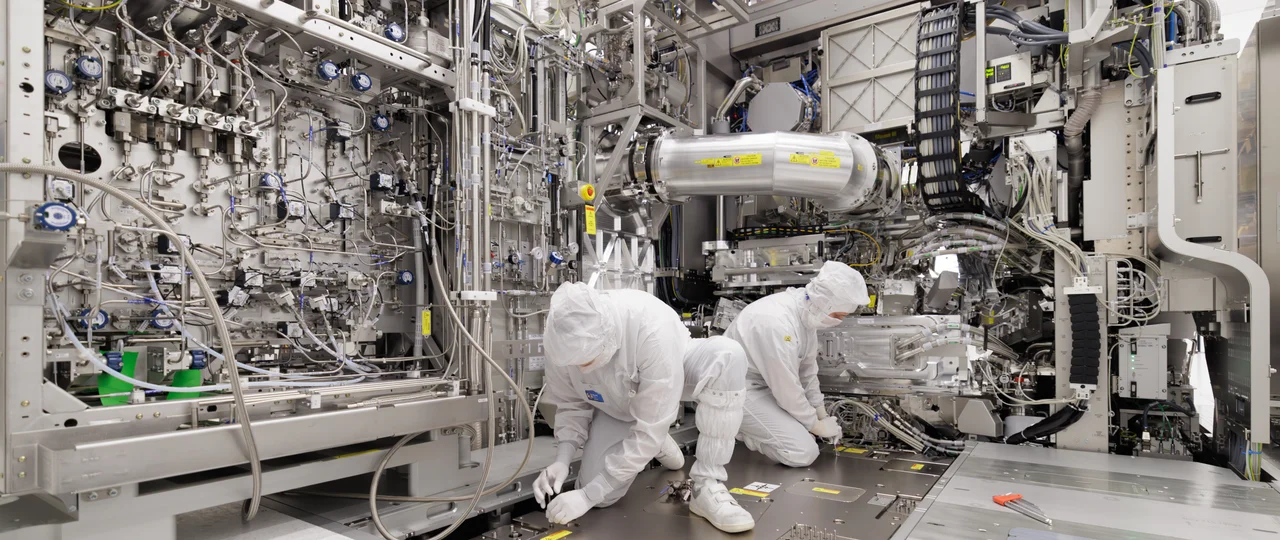

Most notably, some customers have offered to purchase multi-million dollar ASML EUV (Extreme Ultraviolet) lithography machines on behalf of SK hynix to bypass procurement queues. From a data analysis perspective, this indicates a market where the lead time for hardware (often exceeding 24 months for EUV tools) has become the primary constraint on global AI progress, overshadowing software innovation.

The logistical and technical implications of this ‘Pre-paid Infrastructure’ model are immense. Integrating customer-owned equipment into a standardized fab floor plan presents a nightmare for cleanroom certification and process flow consistency. Furthermore, this move signifies the birth of a bifurcated market: an elite tier of ‘hyper-funded’ clients who effectively own dedicated fab lines, and a secondary market of smaller entities forced to survive on the volatile scraps of the general merchant market.

For SK hynix, while this de-risks their massive expansion plans, it also creates an asymmetric power dynamic where major customers may demand granular control over proprietary manufacturing schedules. As we look toward the 2027-2028 cycle, the ability to subsidize a global manufacturer’s production floor will likely become the ultimate competitive moat in the high-end AI economy, turning silicon procurement into a game of pure capital endurance.