🔍 Executive Summary

- Taiwan's AI server supply chain is experiencing a significant expansion as revenue growth spreads from TSMC to peripheral component sectors including advanced cooling, high-spec PCBs, and structural components, signaling a new phase of AI infrastructure scaling.

Strategic Deep-Dive

The narrative of the AI-driven economic boom in Taiwan is undergoing a fundamental shift, moving from a single-actor focus on TSMC toward a comprehensive, ecosystem-wide expansion. April’s sales performance data for the Taiwan electronics cluster reveals that the ’trickle-down’ effect of AI investment is hitting full stride, with record revenues appearing in sectors far removed from pure-play silicon fabrication. While TSMC remains the cornerstone of the industry, the most dramatic relative gains are now being seen in suppliers of liquid cooling solutions, high-performance board materials (CCL/PCB), heavy-duty rail kits, and Baseboard Management Controller (BMC) chips.

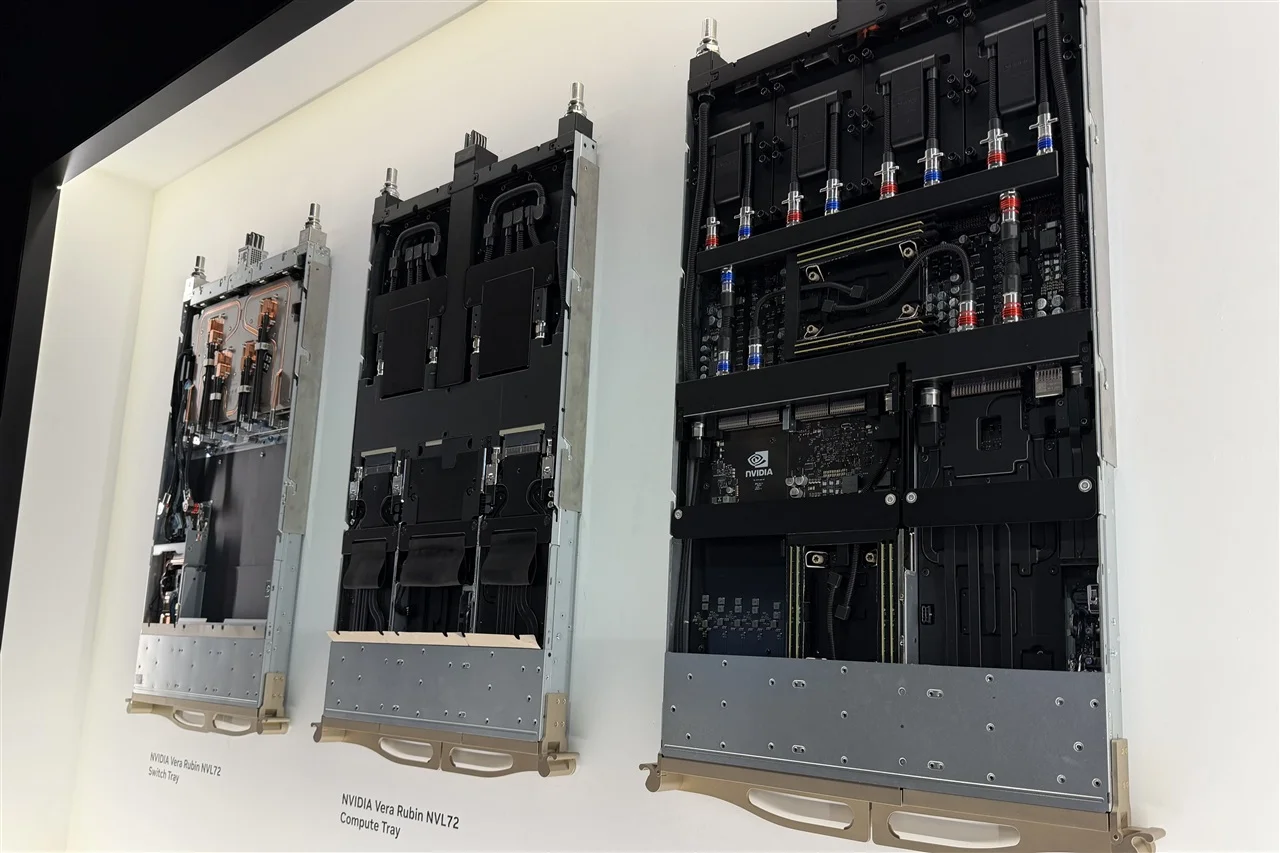

This diversification is the direct result of the unique physical and electrical demands of AI server architecture, which necessitate a complete reimagining of the server’s Bill of Materials (BOM).

From a data architect’s perspective, an AI server is no longer just a high-speed computer; it is a thermal management challenge contained within a structural cage. As power densities for next-generation GPUs approach 1,000W per chip, traditional air cooling is being replaced by sophisticated liquid-to-chip and immersion cooling systems. This transition has turned previously low-margin component categories into high-value engineering segments.

Similarly, the structural integrity required to house dozens of heavy accelerators in a single rack has driven unprecedented demand for specialized rail kits and high-tensile mechanical components. Furthermore, the signal integrity requirements of 800G networking and PCIe Gen6 interconnects have forced a shift toward ultra-low loss PCB materials and high-layer count boards, benefiting Taiwan’s material science leaders. This ‘BOM expansion’ means that for every dollar spent on a GPU, a growing percentage of CAPEX is being allocated to the peripheral hardware that keeps that GPU operational.

Taiwan’s ODM and EMS giants—such as Quanta, Wistron, and Delta Electronics—are at the epicenter of this shift, evolving from simple assemblers into sophisticated system integrators that manage the complex interplay between compute, cooling, and power delivery. This broad-based growth across the supply chain indicates that the AI infrastructure wave is entering a mass-production phase characterized by scale and reliability rather than just experimental performance. For global investors and analysts, the takeaway is clear: the most significant growth opportunities in the next phase of the AI cycle lie in the ‘infrastructure layer’—the specialized components and systems that provide the physical backbone for the world’s growing AI clusters.

Taiwan’s April data isn’t just a snapshot of sales; it is a map of the new AI hardware economy where the ‘peripherals’ are becoming the core.