🔍 Executive Summary

- The 2026 fiscal year marks a definitive pivot in the thermal management industry as escalating AI server power densities drive a massive transition from traditional air-cooling to sophisticated liquid-cooling infrastructures, positioning leaders like AVC and Auras for record-breaking financial performance.

Strategic Deep-Dive

The landscape of the thermal management industry in early 2026 has entered a phase of aggressive divergence, dictated primarily by the evolving requirements of AI-centric infrastructure. As global tech giants accelerate the deployment of next-generation AI servers, the thermal demands of these systems have surpassed the physical limitations of traditional air-cooling methodologies. This transition has created a sharp divide within the Taiwanese supply chain, where companies specializing in advanced liquid cooling and high-performance server thermal solutions are seeing unprecedented growth trajectories, leaving traditional component manufacturers in a state of relative stagnation.

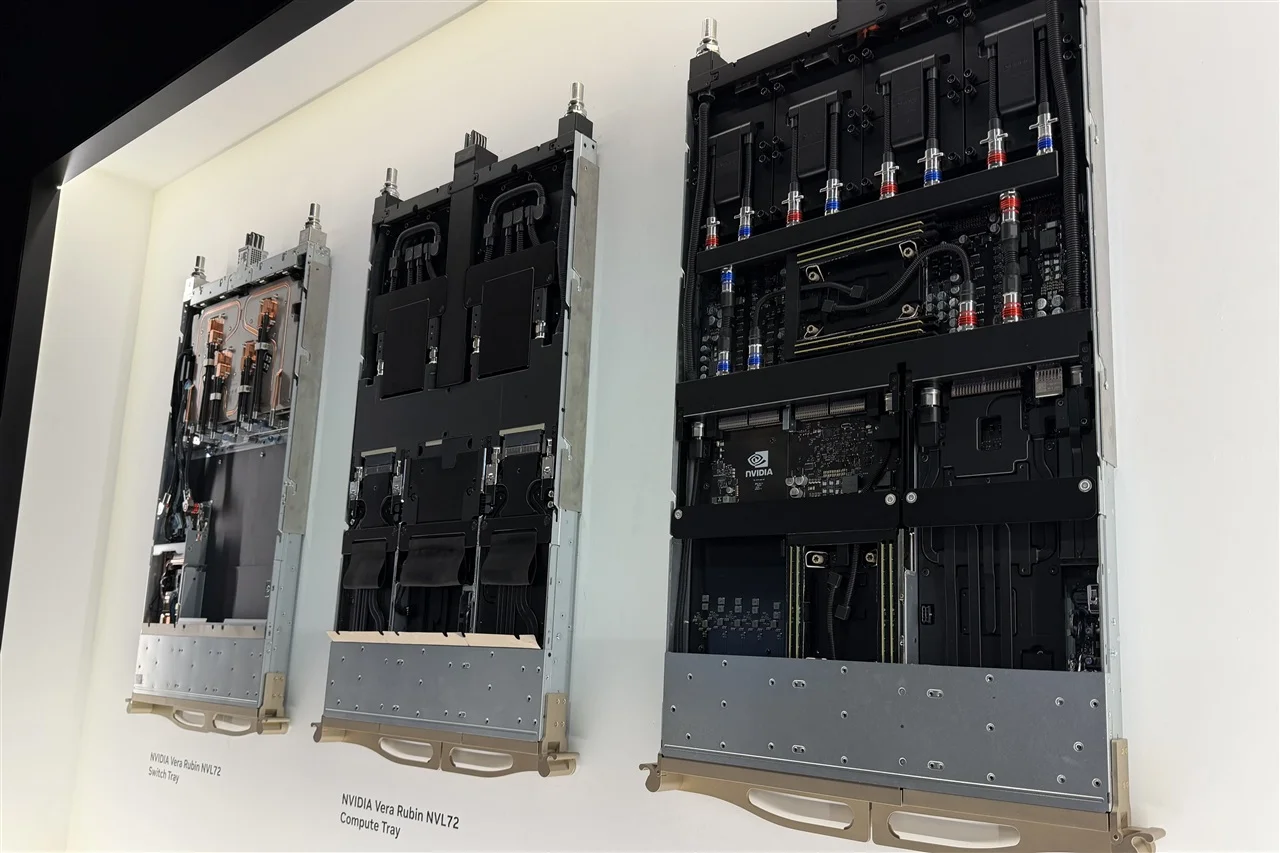

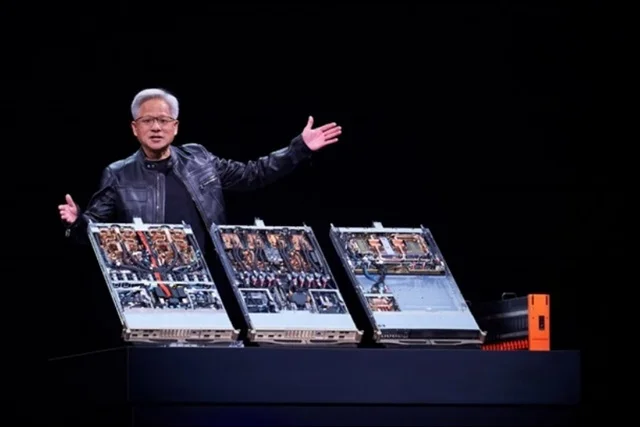

Leading the charge in this 2026 surge are industry stalwarts AVC (Asia Vital Components) and Auras Technology. These firms have successfully pivoted their product portfolios to address the extreme heat flux densities generated by modern AI accelerators and high-performance computing (HPC) processors. The shift to liquid cooling—encompassing cold plate technologies, Coolant Distribution Units (CDUs), and manifold systems—has become the primary driver for their record-breaking revenue figures.

Market data suggests that the adoption of liquid cooling is no longer a niche preference for specialized supercomputers but is becoming a standard requirement for hyperscale data centers aiming to optimize Power Usage Effectiveness (PUE) from historical averages of 1.5 toward the ambitious 1.1 target.

Technically, the divergence is characterized by the increasing complexity of thermal modules. Advanced thermal firms are now integrating more sophisticated materials, such as specialized copper alloys for cold plates and precision-engineered micro-channels, to meet the thermal design power (TDP) demands that often exceed 1,000W to 1,200W per node in the latest server architectures. For AVC and Auras, this shift has facilitated a transition from being commodity component vendors to high-value strategic partners.

They are now deeply embedded in the early-stage ‘design-in’ phases with server OEMs and ODMs, ensuring that fluid dynamics and coolant chemistry are synchronized with chip performance profiles. The financial implications are profound: liquid cooling components command significantly higher average selling prices (ASPs) and superior margins compared to legacy heat pipes and fans.

In contrast, firms that have remained anchored in the legacy PC and traditional enterprise server markets are facing severe pricing pressures. The 2026 surge highlights a clear ‘winner-takes-most’ dynamic in the hardware ecosystem, where early investments in R&D for liquid-to-liquid and liquid-to-air CDU architectures are yielding substantial dividends. As AI models continue to grow in complexity, requiring even more powerful clusters, the demand for sophisticated thermal management is expected to sustain its upward momentum.

This trend further widens the gap between the innovators who can solve the ’thermal wall’ and the traditionalists who remain tethered to declining segments of the global supply chain.