🔍 Executive Summary

- Taiwan's optical module sector reported April revenue of NT$ 2.1 billion, reflecting a complex interplay of month-over-month contraction and year-over-year growth as the market pivots from legacy hardware to high-speed AI networking modules.

Strategic Deep-Dive

Navigating Volatility: The April AI Server and Optical Component Landscape

The April 2026 revenue tracker for Taiwan’s optical module sector provides a nuanced view of the AI-driven infrastructure boom. While the macro-narrative for AI remains overwhelmingly positive, the micro-level data for April reveals a period of “mixed momentum.” The sector generated NT$ 2.1 billion (US$ 66.6 million) in revenue, representing a sophisticated tug-of-war between short-term cyclicality and long-term structural growth.

The Divergence: Understanding the 7.4% MoM Dip vs. 1.2% YoY Gain

To the uninitiated, a 7.4% month-over-month decline might signal a cooling of the AI fever. However, a data systems architect views this through a different lens. Several factors explain this statistical fluctuation:

- Lumpy Project Deployments: High-end networking infrastructure is typically sold in massive, project-based tranches rather than continuous flows. A slight gap between the completion of a major hyperscale data center cluster and the commencement of the next project can cause significant monthly revenue variance.

- Inventory Normalization: Following the aggressive procurement seen in 1Q26, some vendors may be entering a brief phase of inventory adjustment as they clear shelves for the latest 800G and 1.6T module iterations.

- Product Mix Migration: The 1.2% year-over-year increase is the more telling metric. It indicates that the ‘floor’ of the market is rising. Even in a ‘down’ month, the sector is outperforming the previous year’s levels, driven by the higher average selling prices (ASPs) of specialized AI networking components compared to legacy enterprise gear.

Strategic Implications: The Reshaping of Networking Demand

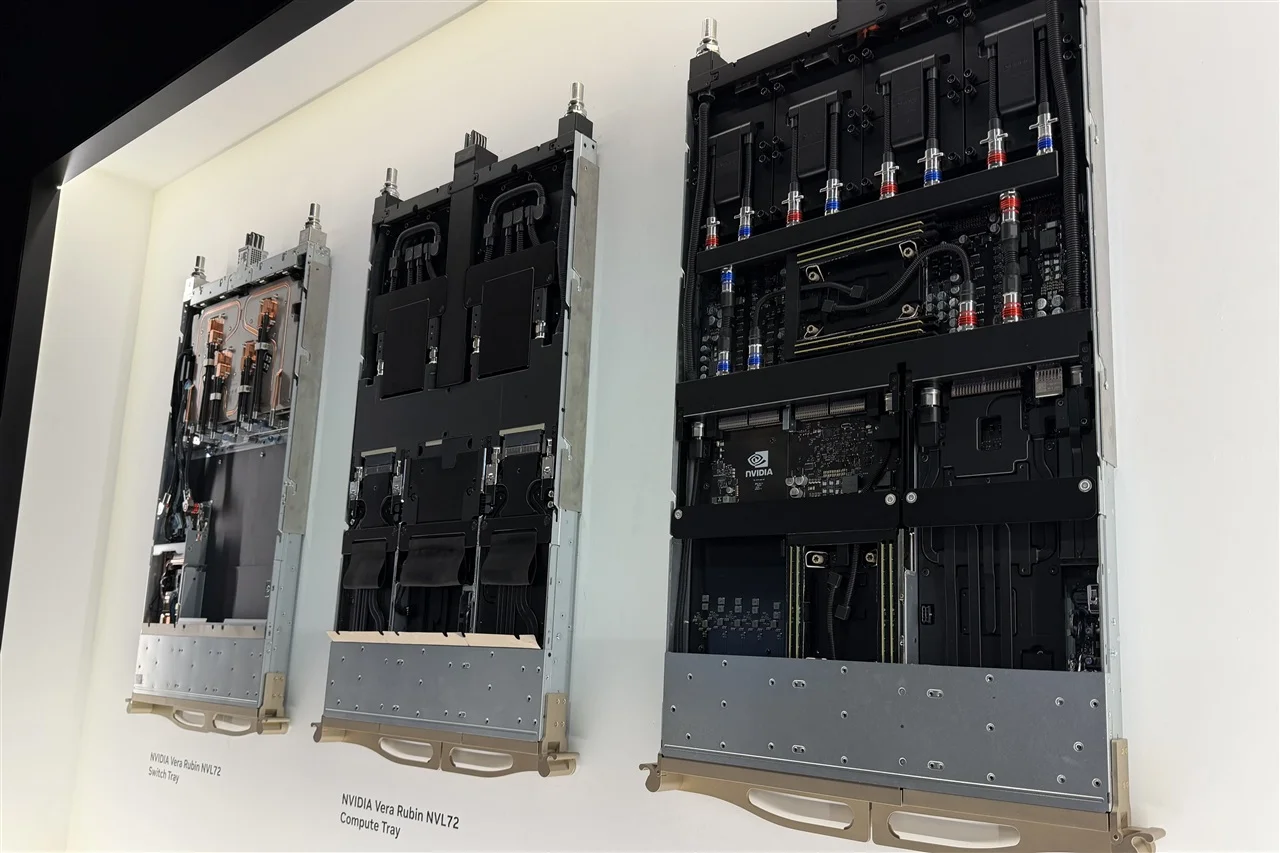

The current market is undergoing a profound “reshaping.” As generative AI models require massive parallel processing across thousands of GPU nodes, the interconnect (the fabric that ties these nodes together) has become the new performance ceiling.

- Standardization on 800G: We are seeing a rapid shift where 400G modules are being sidelined in favor of 800G solutions to minimize latency. Suppliers unable to pivot their production lines to these higher-frequency components are seeing their orders vanish.

- Optical vs. Electrical: Within the server rack, the battle between active electrical cables (AEC) and active optical cables (AOC) continues. The April data suggests that as rack densities increase, optical solutions are gaining favor due to their superior thermal profile and reach, contributing to the sector’s long-term resilience.

In conclusion, while the April figures show a temporary contraction, the cumulative trajectory for the optical module sector remains incredibly robust. The volatility seen this month is a symptom of a high-growth industry rapidly iterating its technological standards. For stakeholders, the focus should remain on those suppliers who are successfully navigating the transition to high-bandwidth, low-latency interconnects, as they are best positioned to capture the next wave of capital expenditure.