🔍 Executive Summary

- Hon Hai Precision Industry (Foxconn) has reported a stellar 63% jump in operating profit for Q1 2026. Despite a seasonal dip in consumer electronics revenue, the company's strategic pivot toward high-margin AI servers and high-speed interconnect infrastructure has driven significant growth and long-term financial stability.

Strategic Deep-Dive

Hon Hai Precision Industry, globally recognized as Foxconn, has unveiled a standout financial report for the first quarter of 2026, headlined by a spectacular 63% surge in operating profit. This robust financial performance serves as a definitive validation of the company’s strategic pivot from its historical reliance on low-margin consumer electronics assembly to becoming a dominant, high-value architect in the Artificial Intelligence (AI) infrastructure sector. According to the detailed figures released via DigiTimes, Foxconn achieved a consolidated revenue of NT$2.11 trillion (approximately US$66.95 billion), signaling its resilience in a volatile global economy.

While the year-over-year revenue growth reached a healthy 29.68%, the report also highlighted a sequential revenue decline of 19% compared to the fourth quarter of 2025. In previous years, such a dip—caused by the typical post-holiday seasonal cooling in the smartphone and PC markets—might have led to concerns over profitability. However, 2026 has marked a structural shift.

The 63% jump in operating profit demonstrates that the margin profile of Foxconn’s current product mix is substantially healthier. The aggressive scaling of AI server production, which involves significantly more complex engineering and higher price points than traditional consumer hardware, has allowed Foxconn to generate more profit from a lower overall revenue base compared to the previous peak quarter.

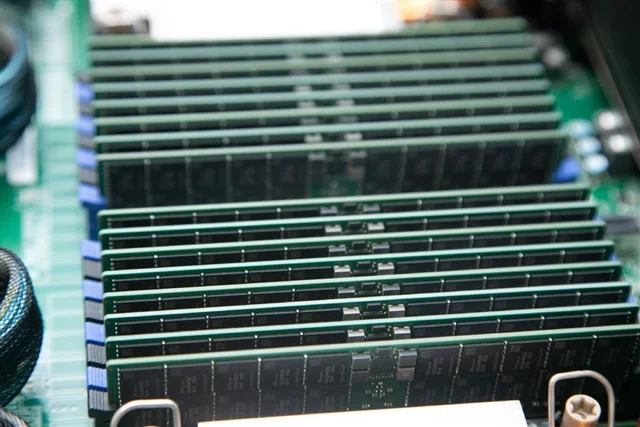

The driving force behind this transformation is the global escalation of AI capital expenditure. As hyperscalers and cloud service providers (CSPs) race to deploy generative AI capabilities, they are increasingly turning to Foxconn as their primary Original Design Manufacturer (ODM). Foxconn has differentiated itself by mastering the integration of advanced server components, including high-speed interconnects and liquid cooling systems, which are now mandatory for high-performance AI clusters.

This specialized manufacturing expertise has created a high barrier to entry, insulating Foxconn from the commoditization seen in other hardware segments. By diversifying its income streams away from a handful of consumer electronics giants, Foxconn is building a more stable, future-proof financial foundation.

Industry analysts believe these results represent a ’new normal’ for global ODMs. The sustainability of the AI boom is no longer in question; it is now the primary engine of industrial growth. Foxconn’s ability to offset a nearly 20% seasonal revenue decline with high-margin enterprise sales suggests that the company is effectively shielded from the traditional cycles of the consumer market.

Looking ahead, Foxconn is expected to continue investing in advanced manufacturing technologies, such as automated assembly for modular server designs and high-speed signal integrity testing. These investments are critical for maintaining its lead in the AI server market share. As enterprises worldwide move from AI experimentation to full-scale integration, Foxconn remains at the center of the hardware ecosystem, poised to capture the next wave of infrastructure spending.

For investors, the takeaway is clear: Foxconn is no longer just an iPhone assembler; it is the backbone of the AI era, providing the essential physical infrastructure that powers the digital future.