🔍 Executive Summary

- China's leading memory manufacturers, YMTC and CXMT, are aggressively expanding their NAND and DRAM production capacities to capitalize on the AI-driven demand surge while navigating international trade restrictions.

Strategic Deep-Dive

The Chinese memory semiconductor industry is pivoting into a high-intensity expansion phase, led by the aggressive capital expenditures of Yangtze Memory Technologies (YMTC) and ChangXin Memory Technologies (CXMT). This strategic escalation is fueled by a dual-engine motivation: the unprecedented global demand for memory generated by the generative AI revolution and a national imperative to achieve technological self-sufficiency amidst tightening Western export controls. As artificial intelligence models grow in complexity, the hardware requirements for both training and inference have shifted the demand curve for NAND flash and DRAM into a state of structural deficit, providing a unique market entry window for Chinese champions.

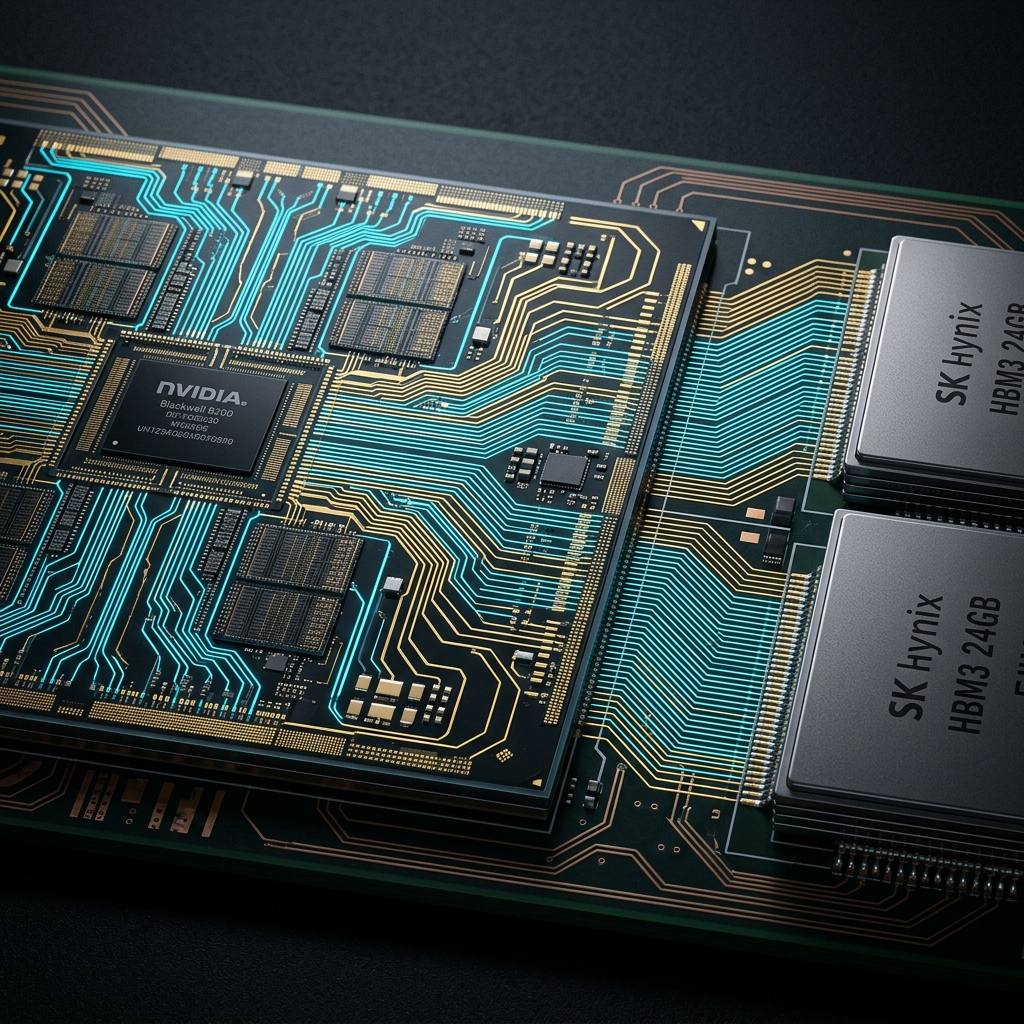

YMTC is currently focusing its strategic efforts on its proprietary Xtacking architecture, aiming to refine the mass production of 232-layer and beyond NAND flash memory. By stacking the memory cells and logic circuitry on separate wafers before bonding them, YMTC has achieved performance levels that rival global leaders, positioning itself as a critical supplier for high-speed AI storage solutions. Simultaneously, CXMT is making significant strides in the DRAM sector, transitioning from legacy DDR4 nodes to advanced LPDDR5 and exploring the high-bandwidth memory (HBM) architectures that are essential for next-generation AI accelerators.

The current expansion phase involves not just the acquisition of domestic and authorized international lithography tools, but a massive scale-up of fab footprint in key industrial clusters within China.

The strategic implications of this investment surge are profound. By ramping up investments in DRAM and NAND, YMTC and CXMT are responding to the tightening supply conditions that have characterized the global market since the industry-wide production cuts of 2024. These companies are effectively leveraging the ‘AI vacuum’ to establish a more robust presence in the global semiconductor hierarchy.

Analysts suggest that this expansion is multifaceted; it serves to protect domestic supply chains from geopolitical volatility while simultaneously challenging the pricing power of traditional market incumbents. As global markets grapple with supply constraints, China’s domestic memory champions are positioning themselves as an alternative, yet increasingly sophisticated, pillar of the global electronics ecosystem.

Looking toward 2027, the success of these initiatives will likely dictate the balance of power in the memory supply chain. If YMTC and CXMT can maintain their technological momentum while scaling output, they will become indispensable to global AI infrastructure, regardless of geopolitical friction. The current phase of expansion marks a pivotal moment for the industry, as the focus shifts from mere manufacturing to the mastery of the high-speed data interconnects that define the AI era.

This movement reflects a concerted effort by the Chinese state to transform its semiconductor sector into a central hub for the critical memory technologies that underpin the modern digital economy.