🔍 Executive Summary

- GB300 has emerged as the primary driver for AI server ODM revenue in Q1 2026.

- The upcoming Vera Rubin architecture is expected to ramp in Q3 2026.

- Cloud service providers are increasing proprietary ASIC deployments alongside Nvidia hardware.

Strategic Deep-Dive

The AI computing landscape in early 2026 is defined by the strategic consolidation of the GB300 series and the looming shadow of the Vera Rubin architecture. As of Q1 2026, the GB300 has become the operational backbone for global hyperscalers, driving a massive revenue tailwind for ODMs. Architecturally, the GB300 represents the refined peak of the Blackwell generation, utilizing enhanced HBM3e stacks and optimized power management integrated circuits (PMICs) that allow for higher compute density within existing rack power envelopes.

This has allowed enterprises to scale their inference capabilities without a total overhaul of their data center infrastructure.

However, the industry’s strategic focus is rapidly shifting toward the Q3 2026 launch of the Vera Rubin platform. This transition is not merely an incremental update; it represents a significant leap in system-level architecture. Rubin is expected to be the first widespread implementation of HBM4 memory, necessitating a redesign of memory controllers and interposer technologies.

Furthermore, the thermal demands of Rubin-class GPUs are pushing the industry toward a mandatory adoption of advanced cooling solutions. We are seeing a decisive move from traditional air-cooling to closed-loop liquid cooling (DLC) and immersion systems, creating new opportunities for component suppliers specializing in pumps, manifolds, and quick-disconnect couplings.

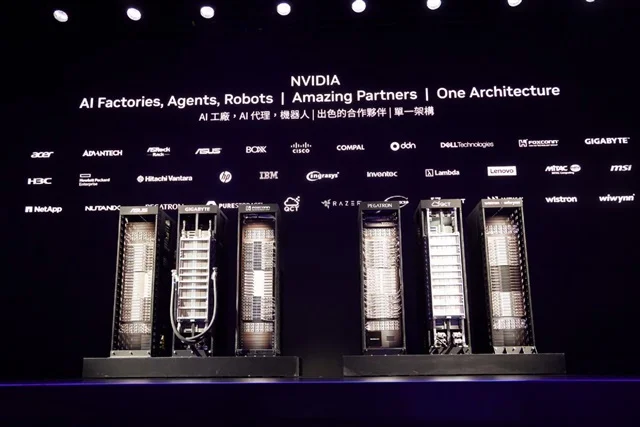

Simultaneously, we must address the rise of cloud-native ASICs (Application-Specific Integrated Circuits). While titans like AWS (Trainium/Inferentia) and Google (TPU v6/v7) are accelerating their internal silicon deployments to optimize total cost of ownership (TCO), they remain heavily reliant on Nvidia for the bulk of their general-purpose AI workloads. The GB300 and the upcoming Rubin are viewed as the ‘gold standard’ for flexibility and raw performance.

The supply chain is currently managing a delicate balancing act: clearing GB300 inventory to make way for Rubin while supporting the parallel growth of CSP-specific ASIC production. This dual-track growth ensures that the Taiwanese manufacturing ecosystem, which handles both Nvidia’s reference designs and custom ASIC production, remains the ultimate beneficiary of the AI infrastructure boom.