🔍 Executive Summary

- The rapid expansion of AI-driven data centers is redistributing economic power in East Asia, with Taiwan emerging as the primary architect of the AI server backbone while South Korea grapples with the risks of domestic industrial decline.

Strategic Deep-Dive

The global surge in artificial intelligence adoption has triggered a massive capital expenditure cycle centered on data center infrastructure, a trend that is fundamentally reconfiguring the export hierarchies of East Asian economies. As hyperscalers like Microsoft, Google, and Meta aggressively scale their AI capabilities, the demand for specialized AI servers has become the primary engine of trade growth. However, this ‘AI Gold Rush’ is not distributing wealth evenly.

Instead, it is redrawing the global export map, creating a distinct divergence between nations that have integrated into the high-value AI hardware stack and those still tethered to legacy manufacturing paradigms.

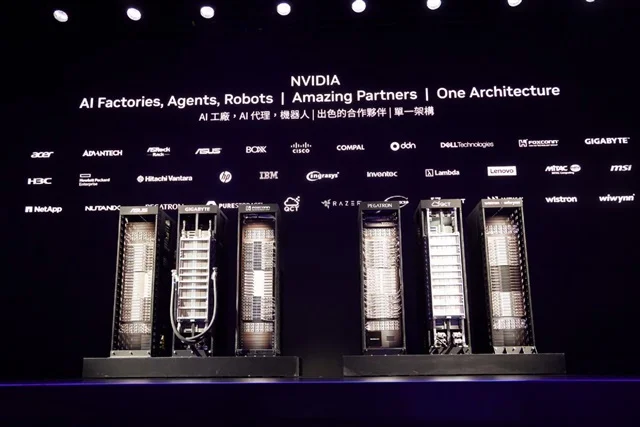

Taiwan has positioned itself as the indispensable architect of this new era. Beyond its well-known dominance in advanced logic chips via TSMC, Taiwan has successfully leveraged its robust electronics manufacturing services (EMS) ecosystem to monopolize the AI server assembly market. Companies such as Quanta Computer and Foxconn are no longer just assemblers; they are strategic partners providing sophisticated thermal management, power distribution, and high-speed interconnect solutions for AI data centers.

The concentration of CoWoS packaging capacity within Taiwan’s borders has created a powerful gravity well, pulling global investment and supply chain logistics toward the island. Consequently, Taiwan is experiencing a structural boom, with its export profile shifting from consumer electronics to high-margin industrial infrastructure, effectively future-proofing its economy against cyclical downturns.

In contrast, South Korea is sounding a strategic alarm regarding a potential ‘manufacturing hollow-out.’ Despite its undisputed leadership in High Bandwidth Memory (HBM), the broader South Korean industrial base is struggling to capture the full value of the AI server boom. The concern is that while South Korea provides the ‘memory cells,’ it is excluded from the high-value system integration and chassis manufacturing that Taiwan dominates. This disparity is exacerbated by domestic factors, including rising energy costs and a rigid regulatory environment, which have incentivized Korean firms to move their sophisticated manufacturing operations abroad.

This migration of the industrial base threatens to leave the domestic economy hollowed out, characterized by a lack of high-quality industrial jobs and a diminishing role in the physical assembly of the AI era’s most critical assets. The current export data suggests that South Korea’s reliance on commodity-like memory cycles makes it vulnerable to the volatility of the tech market, whereas Taiwan’s grip on the server backbone offers a more resilient and lucrative economic path. To reverse this trend, South Korea must move beyond its ‘memory-first’ mentality and foster a domestic ecosystem for AI system integration, cooling technologies, and specialized power management chips.

The redrawing of the export map serves as a stark reminder: in the AI economy, being a component supplier is good, but being the platform integrator is transformative.